Hiring Disabled Workers in China: Incentives and Challenges

By Samuel Wrest

The fallout from China’s abolishment of its one-child policy has taken new and unexpected turns in recent weeks. Following protests from parents affected by the 36 year old policy – most by having a single disabled or severely ill child unable to support them in their old age – the government stated that it would increase the monthly subsidy for families whose only child is disabled. The announcement has been widely reported in Western media and has helped reenergize discussion of the role that the disabled have in Chinese society, particularly in the workforce.

When China hosted the Paralympic games in 2008, then president Hu Jintao promised that the country would strive to make its disabled citizens “equal members of society”, a statement that presaged a string of national and provincial policies aimed squarely at incentivizing businesses to hire disabled workers. Awareness of these incentives among foreign companies, however, has remained generally low since their implementation, and many domestic companies choose not to use them – two factors in many that have seen a low employment rate for China’s disabled citizens.

What incentives exist for hiring disabled employees?

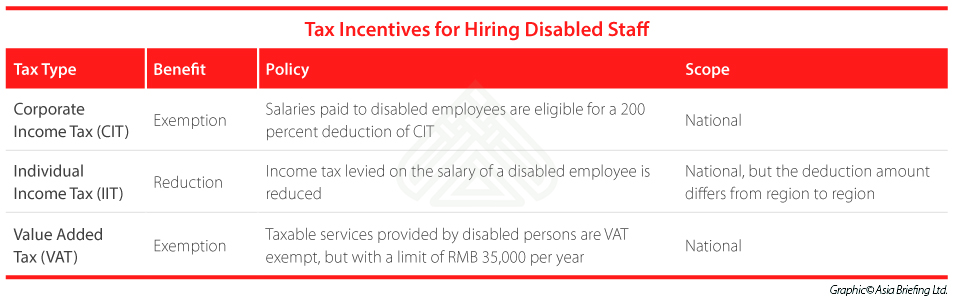

The preferential policies that exist for disabled workers in China mainly revolve around tax breaks or exemptions. However, the ease with which companies can qualify for these benefits varies, with eligibility often hinging on either the size or the location of the company. Below, we take a closer look at the three main preferential policies.

Corporate income tax

The way in which the CIT exemption for disabled employees functions is noteworthy. In China, companies can deduct a non-disabled employee’s annual salary from the profits that they pay CIT on. For disabled employees, this amount is doubled. If a disabled employee’s annual salary is RMB 100,000, for instance, then the company will be able to deduct RMB 200,000 from the amount that it pays CIT on.

In order to qualify for this benefit, companies must meet all of the following requirements:

- The disabled employee must have a minimum one year labor contract or service agreement with the company;

- The company must pay the monthly social security costs for the disabled employee;

- The disabled employee’s salary cannot be any less than the lowest salary paid to a non-disabled employee in the company.

![]() RELATED: Payroll and Human Resource Services

RELATED: Payroll and Human Resource Services

Individual Income Tax

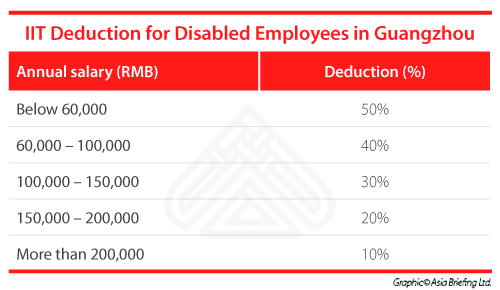

While disabled persons employed anywhere in China are eligible for IIT deduction, China’s tax authorities have yet to implement a nationwide standard. The deduction amount therefore varies from region to region, with the country’s more affluent areas tending to provide greater deductions. Below, we provide an example in Guangzhou, Guangdong province.

VAT

The requirements to qualify for VAT exemption are extensive. Not only must 25 percent of a company’s workforce be disabled, but the company must also have a minimum of ten disabled employees. In practice, this means that the exemption is only available to larger companies. If the workforce of a small startup with 16 staff were 50 percent disabled, for example, they would still be ineligible for the VAT exemption.

In addition to this provision, the conditions for qualifying for CIT exemption also apply for VAT exemption.

Quota for hiring disabled employees

The Chinese government has actually set a minimum quota of disabled employees that a company must hire. The national average is 1.5 percent of a firm’s workforce, but the rate can differ by province. The quota does not apply to companies under three years old and with a workforce of less than 20.

Companies that don’t meet this quota have to pay into a fund called the Baozhang Jin (保障金). The necessary amount again varies according to location, but the majority of companies choose to pay into the fund rather than employ the requisite amount of disabled workers that would absolve them from paying. Reluctance to train disabled staff and integrate them into the company structure is a commonly cited reason for this, but the fact that few companies choose to take advantage of the Baozhang Jin’s exemption is one of the root causes of China’s low disabled employment rate.

How is ‘disability’ defined in China?

The Law on the Protection of Disabled Persons (LPDP) is China’s primary piece of legislation on disability rights. In its second Article, the Law describes a disabled person as someone who “suffers from abnormalities or loss of a certain organ or function, psychologically or physiologically, or in anatomical structure and has lost wholly or in part the ability to perform an activity in the way considered normal.” The law further states that the term “disabled person” refers to those with “visual, hearing, speech or physical disabilities, mental retardation, mental disorder, multiple disabilities and/or other disabilities.” Importantly, it notes that the “criteria for classification of disabilities shall be established by the State Council”.

Looking ahead

The incentive framework that China has put in place for hiring disabled employees has been incremental since Hu Jintao’s speech at the Paralympic games. Policies such as the Baozhang Jin have been revised and implemented as recently as October 2015, and China is still catching up with some of its international commitments regarding disabled employment, such as those contained in the International Labor Organization’s conventions on employment and education for the disabled that China ratified in 1985.

This suggests that more change can be expected in both the short and long term future, with China developing a policy framework that supports its public and international backing for disabled employment and further incentivizes China-based businesses to hire disabled workers.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

Human Resources and Payroll in China 2015

This edition of Human Resources and Payroll in China, updated for 2015, provides a firm understanding of China’s laws and regulations related to human resources and payroll management – essential information for foreign investors looking to establish or already running a foreign-invested entity in China, local managers, and HR professionals needing to explain complex points of China’s labor policies.

Establishing & Operating a Business in China 2016

Establishing & Operating a Business in China 2016

Establishing & Operating a Business in China 2016, produced in collaboration with the experts at Dezan Shira & Associates, explores the establishment procedures and related considerations of the Representative Office (RO), and two types of Limited Liability Companies: the Wholly Foreign-owned Enterprise (WFOE) and the Sino-foreign Joint Venture (JV). The guide also includes issues specific to Hong Kong and Singapore holding companies, and details how foreign investors can close a foreign-invested enterprise smoothly in China.

Labor Dispute Management in China

Labor Dispute Management in China

In this issue of China Briefing, we discuss how best to manage HR disputes in China. We begin by highlighting how China’s labor arbitration process – and its legal system in general – widely differs from the West, and then detail the labor disputes that foreign entities are likely to encounter when restructuring their China business. We conclude with a special feature from Business Advisory Manager Allan Xu, who explains the risks and procedures for terminating senior management in China.

- Previous Article Labor Case Study: Social Insurance Contribution in China

- Next Article A Guide to Consumption Tax in China