China Incorporations. Let’s Get Real: They are a Tax-Based, not Legal, Structure

Op-Ed Commentary: Chris Devonshire-Ellis

Jul. 5 – One of the key issues of truly understanding foreign investment into China is the recognition that it is tax structuring, rather than the local legal structures, that dictate the success or failure of the investment. China’s legal administration laws – for that is all we’re really talking about when it comes to RO/FICE/WFOE/JV structures – are fairly well organized and make sense. The regulatory framework supporting them is in place and has been tested many times over the past 25 years.

Many overseas lawyers or basic incorporation businesses like to talk up the bureaucratic and legal aspect of the incorporation process, and often are doing so to talk up fees or the difficultly of the work involved. Yet the legal administrative structure in obtaining a business license to operate in China as a foreign investor is so well thought out and easy to follow that our firm has been publishing the entire procedural flow charts for incorporation procedures for many years.

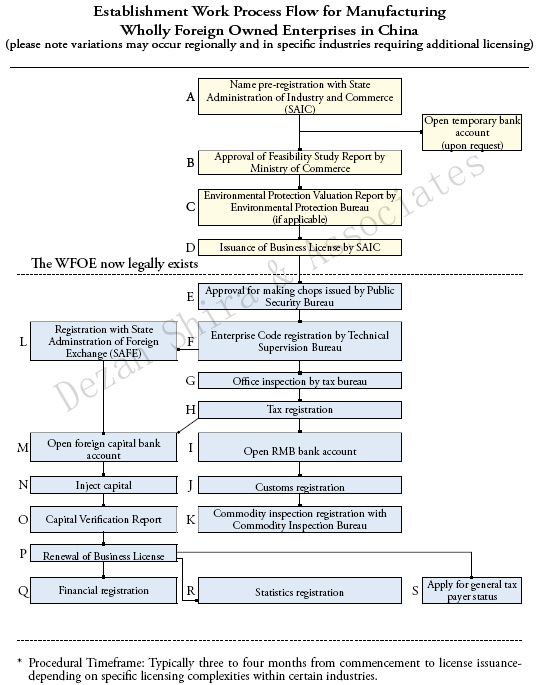

Here’s an example for a WFOE:

In fact, legal incorporation work is so simple in China that it does not even require a licensed law firm, foreign or otherwise, to conduct this work. Hence the many Chinese consultants and even government foreign investment fast-track departments that will assist in taking investors through the process. The trick with incorporating in China is not therefore the well-trodden legal administrative procedure. The real deal is getting the financing right, and it’s here that the average foreign law firm or incorporation consultant advising overseas clients in China gets out of their depth.

There are a number of pitfalls that the unprepared or ill-advised foreign investor can fall into when it comes to the financial aspect of preparing an investment into China, and the importance of these far outweigh the legal administration aspect of incorporation. Simply put, placing too much attention on an already well-defined application procedure can lead to completely missing the real structural processes that are required when incorporating a business in China. Here we list some of the financial issues that are commonly overlooked – often because foreign law firms are not aware of them:

Sending start-up funds to somebody else before the license is issued

It takes normally four to six months to complete a China incorporation application, however, some foreign investors can’t wait that long and try to send the start-up funds to their local agent or local staff to cover the cost for the initial office fit-out, overhead or even equipment purchases. The problem is that these funds, as paid for the setup procedure, cannot be recognized as part of your capital injection once the business license is issued, as the capital injection has to be transferred by the foreign investor from their overseas account to the nominated capital account directly, and not via any third party.

We have previously had clients remitting up to US$200,000 to their local supplier asking them to pay for rental and purchase equipment prior to the license being issued, with them subsequently finding it very difficult for them to pursue the balance and show such purchases as part of their capital injection. Rather, it is better to open a temporary capital account right after the name registration is completed. If you don’t handle this properly, the start-up fund sent before WFOE incorporation could be hard to be recognized registered capital, and it won’t be easy to repatriate back to HQ after the registered capital is met in full as well due to Forex control in China.

Registered capital issues: Undercapitalization

One of the most common, and most serious, problems with FIE applications, especially for small businesses, is the issue over registered capital. This is a much misunderstood area. Confusion exists, and many ill-advised investments are made in China due to misinterpretation of the local governments term “minimum registered capital.” This is not supposed to be a ruling on how much you need to invest. Actually, the amount of registered capital needed in the business depends on a number of different factors.

Location – Some regions in China apply different levels of capital requirements than others to reflect their lower or higher regional operational costs.

Scope of business – For certain industries or services, the applicable registered capital amount can be quite high. This is sometimes used as a protectionist tool to discourage foreign investment, and is sometimes used to ensure that only the right standard of international business can enter the market to ensure the quality of the applicant. Note that if some existing businesses wish to expand their current scope of business, it may be required to increase the amount of registered capital.

Cash flow – This is critical and often overlooked. Registered capital is also required to fund business operations until it is in a position to fund itself. Generally speaking this should be catered for in the feasibility report – a business plan type document that is submitted to the authorities as part of the application process. In the rush to attract new investments many government agents do not pay much attention to details of this report. Often the happy foreign investor will naively assume he’s gotten a great deal due to “minimum amounts” being identified as all that is required. However, the business can come to a shuddering halt if the registered capital amount is insufficient to support the operations cash flow. It is also not just a simple matter of wiring additional funds to China.

The procedures to be followed include:

- Application to increase the registered capital with the original licensing authority

- Application to the State Administration of Foreign Exchange to transfer funds into China bank to fund transfer

- Capital verification

- Reissuing of business license reflecting above; this is important as the registered capital amount is also the limited liability status of the business

- Update other licenses at various government authorities for registered capital amount

These steps take between six to eight weeks to fulfill. If you have already run out of operational money, you by now have not paid your staff, your suppliers, and possibly your utilities for two months. In effect, your business has been throttled before it even had a chance to breathe. It is vital you properly capitalize your business in China in accordance not just with government guidelines over “minimum registered capital,” but also with regards to pure economic and operational realities.

Businesses can and do go broke in China because of this issue, and unscrupulous consultants may not always advise on the matter as they seek to gain more fees from you in terms of sorting the problems out when they arrive, or because they are just in the business to make a quick buck out of handling your registration processes without putting any thought into the business aspects of your operations. The catch here is that if you do run out of cash flow due to undercapitalization, you can wire money to the businesses capital account. In doing so, China’s tax bureau will regard this as taxable income, meaning you incur an additional tax bill purely for refinancing your business. It’s an obvious waste. Calculating the required registered capital properly in advance will save a lot of headaches and an unnecessary loss of capital later on.

Maintaining currency consistencies in the articles and business license

When applying for your business license, it is important to pay attention to detail when completing the application and cross-referencing this against the articles. If, for example, the capital amount to be registered on their business license is shown in RMB, it can cause issues if the AOA identifies this amount in euros or U.S. dollars. Consequently, if the exchange rate fluctuates, the injection verified by the local CPA firm as is required to prove the registered capital transfer, may no longer match the figures on the business license. The registered capital converted into RMB may be less than their promised capital amount. So, the client has to transfer again, bearing the uncovered missing amount caused by currency fluctuations into their capital bank account. They also have to complete another capital verification, which is an annoyance and wastes the investor’s money and time.

Keeping the legal and operational address of the FIE the same

Many smaller consultants and agents in China may advise investors that it is permissible for the FIE to register in one location (in a small office building for example), but then have its manufacturing facility setup in a different location (rural country side). This may be to take advantage of better profits, tax rates or other incentives in the office location area, yet effectively operate from a different location. If so, this does cause trouble for post-registration procedures such as environmental appraisal and VAT application. This point is often missed by consulting firms and certain lawyers who do not provide post-registration work. It can have serious effects on the client and possibly make their business unworkable.

Important tax issues that are commonly misjudged

VAT treatment

There are many common misconceptions as concerns to VAT exemption on exports. If the refund rate is lower than the levy rate, the company must bear the additional VAT cost on exportation.

The VAT rate for general taxpayers is generally 17 percent, or 13 percent for some goods. For taxpayers who deal in goods or provide taxable services with different tax rates, the sale amounts for the different tax rates shall be accounted for separately. If this is not done, the higher tax rate applies.

The VAT cost is calculated as follows:

VAT general taxpayers

The VAT payable shall be the balance of output tax for the period, after deducting the input tax for the period. The formula required:

VAT payable = output VAT – input VAT

Output VAT is calculated based on the value of the taxpayer’s sales, namely Output VAT = A × B, where A = sales value and B = tax rate

For the sale of goods or taxable services, VAT is incurred on the date when the sales sum is received, or documented evidence of the right to collect the sales sum is obtained. For imported goods, it is incurred on the date of import declaration. VAT on imported goods is collected by China Customs on behalf of the tax authorities. VAT on articles for personal use brought or mailed into China by individuals is levied at the same time as customs duty.

Customs deposit on imported raw materials to be subsequently exported

We often hear the misconceived statement: “There is no VAT and custom duty levied on imported raw materials used for manufacturing goods locally if these are then finally exported 100 percent.” It is incorrect.

Actually, newly established foreign-invested enterprises must still make a tax deposit to the Administration of Customs for VAT (at around 17 percent) and remit duty on the initial importation, generally for a period of six months. Many new businesses do not budget for this as initial working capital to be contributed as part of registered capital, leaving them short of operating cash later on.

Enhanced profits repatriation: reducing taxes in your business

This is a tax issue, and applies to all FIEs that sell services or products in China. Foreign-invested enterprises, as mentioned earlier, are not just simple licensing applications and, if you treat them as such, you end up with an inefficient business. A company can significantly enhance profitability by reducing profits tax burden by essentially making sure to introduce into the business a series of allowable service contracts between the FIE and its parent company back home.

These services can include:

- Royalties such as for trademark and patent use

- Interest on loans

- Rental income

Royalties, interests and rental income rendered to the FIE in China generally attracts a withholding tax at a rate of 10 percent. That means, if the income derived from above mentioned activity is US$1,000, a foreign-invested enterprise located in China will withhold US$100 income tax. This compares favorably against the profits tax authorities at the yearend, who can be more avaricious. If the money is left in the company, the profits tax authorities will levy rates of 25 percent corporate income tax. To take advantage of this, an enhanced profits repatriation structure needs to be built into the FIE articles and inserted (they do not appear in normal drafts), and a series of contracts agreed between the parent and the foreign-invested enterprise, and registered with the tax authorities in China for assessment.

Other post-registration procedures

The paperwork does not stop there. You still have quite a bit to do before you have a fully efficient business.

This additional work consists of:

- Approval for making chops by Public Security Bureau

- Enterprise code registration with the Technical Supervision Bureau

- Office inspection by the tax bureau

- Tax registration

- Opening an RMB bank account

- Customs registration for import-export license

- Commodity inspection with Commodity Inspection Bureau

- Registration with the State Administration of Foreign Exchange

- Opening foreign capital bank account

- Injection of capital and capital verification report

- Renewal of business license by SAIC after capital has been injected

- Financial registration

- Statistics registration

- Application for general tax payer status

Note that many consultants and law firms do not regard post registration procedures as part of their scope of work when processing clients’ applications, so either shop around for a firm that does or ensure you have this vital component catered for elsewhere. Not following through correctly on these procedures can lead you to non-compliance and government penalties later on.

As can be seen, tax and finance are therefore an important part of any application for any business in China. Other aspects can also crop up, such as location issues, use of free trade zones, bonded warehouses, labor law, and of course issues concerning the articles of association. China also has numerous double tax treaties in place with an increasing number of countries that may also impact favorably on WFOE tax planning, while subjects such as holding company structuring should also be considered as part of the tax aspect.

Inter-company aspects such as reducing profits tax in China through structuring royalty agreements and so on should also be considered. The provision of simple applications or standard documentation for WFOE applications is not going to be enough when wanting to professionally establish a business capable of operating to its complete financial potential in China. Attention to detail must be paid to finance and tax, and ignoring or discounting the importance of these issues leaves the investor with a crippled corporation.

Chris Devonshire-Ellis is the principal of Dezan Shira & Associates. The practice has been operational in China since 1992 and provides legal administration, establishment and tax planning services, in addition to ongoing compliance and maintenance issues with customs, tax and labor law to investors in the China market. The firm has 12 China offices. Please visit the firm’s web site, e-mail the firm for advice on China WFOE structuring at legal@dezshira.com, or download the firm’s brochure here.

Related Reading

China Briefing Magazine: Establishing FICE in China (New Issue)

China Briefing Magazine: Establishing FICE in China (New Issue)

In which we discuss trading in China, and the incorporation of foreign-invested commercial enterprises – the most commonly used form of wholly owned foreign investment for trading in China. Priced US$10.

Setting Up Wholly Foreign Owned Enterprises in China (New, Third Edition)

Setting Up Wholly Foreign Owned Enterprises in China (New, Third Edition)

Our complete, 94 page guide to the entire process of establishing a WFOE in China, including pre-incorporation planning, articles of association, full financial and tax implications, the application process, and on-going operational and compliance issues. Priced US$40.

Asia Double Tax Treaties 2011

Asia Double Tax Treaties 2011

Dezan Shira & Associates’ guide to all Asian tax treaties including those for China. Indispensible intelligence for structuring cross border investments from overseas into China.

It’s Now Time to Upgrade your RO to a WFOE

- Previous Article China Renewable Energy Industry Update: Jul. 5

- Next Article China’s Second Tier Cities – the New Kids on the Block